%201.svg)

Navigating Chargeback Regulations: What eCommerce Merchants Need to Know

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

Learn how eCommerce merchants can navigate chargeback regulations, prevent losses, and stay compliant in this essential guide.

Chargeback rules in the U.S. and the U.K. have been in place since the 1970s to protect consumers from losing money due to clerical mistakes, explicit misrepresentation, or fraud on their credit cards.

Because chargeback regulations are mainly meant to protect consumers' interests, merchants are often at the mercy of customers who abuse these chargeback regulations. In addition to lost sales, chargebacks incur the merchant's processing fees for every dispute—not to mention the business's bad reputation with its payment processors and customers.

In this article, let’s switch the lenses and see how chargebacks impact eCommerce merchants—everything you need to know about chargebacks, the regulations related to the chargeback process, and how to stay compliant while managing these customer disputes.

What Is a Chargeback?

A chargeback is a dispute made by a customer against the eCommerce merchant or the bank to reverse a transaction made through a debit or credit card purchase. It happens when a customer complains about the transaction, its delivery, or your products or services and requests a refund of the amount charged to their funds.

While it sounds simple, chargebacks can be long and complicated processes involving documentation, confirmation, and examination by several parties, including the issuing bank, the acquiring bank, the processor, and the card network.

A simple step-by-step process of a chargeback process involves the following:

- A customer reaches out to the issuing bank to dispute a transaction.

- The issuing bank examines the validity of the complaint. If it is invalid, the bank will take no action. If the issuer accepts the complaint, the customer will receive a temporary credit to their account.

- The issuing bank will then forward the chargeback to the merchant’s acquiring bank, and the merchant can accept or contest the chargeback.

- If the merchant accepts the chargeback, they will be charged the full amount plus additional chargeback fees.

- A merchant who decides to contest the chargeback will send evidence and relevant documentation to the acquiring and issuing bank, which may then proceed to the pre-arbitration and arbitration phase.

Jonathan Feniak, General Counsel at LLC Attorney, says, “When a chargeback reaches the final arbitration phase, the card processor (Mastercard, Visa, etc.) decides on the dispute. The party responsible (the merchant or the cardholder) can be hit with fees reaching thousands of dollars.”

When Do Chargebacks Happen?

Understanding when a customer can file for a chargeback is important in determining how to proceed and win a transaction dispute. Here are some of the most common causes of a chargeback:

- Credit or debit card fraud: A customer can initiate a chargeback when an unauthorized transaction on a cardholder’s account causes them to lose money through a fraudster who obtains a cardholder’s card information to make purchases. After the bank examines the claim, a cardholder can file a chargeback for unauthorized purchases.

- Merchant or customer errors: Merchant or customer errors can result from duplicate charging or processing errors, such as incorrectly charging customers the wrong amount.

- Canceled and returned transactions: Without a return policy, it is inevitable for merchants to experience disputes and chargebacks from customers who choose to cancel or those who are dissatisfied and return their purchases.

- Fulfillment failures: Order fulfillment is a crucial part of the sales process and greatly affects a customer’s satisfaction. Failed delivery, late delivery, or incorrect or missing items can trigger a customer to cancel the entire order and demand a chargeback.

- Friendly fraud: Also called chargeback fraud, this type of fraud occurs when a customer purposely misrepresents a legitimate transaction as a fraudulent one, initiating the chargeback process. This type of fraud accounts for 70% of all credit card frauds, costing $132 billion annually.

What Are the Chargeback Regulations eCommerce Merchants Need to Know?

With chargeback laws mainly favoring the consumers rather than the merchants, eCommerce merchants need to be aware of specific chargeback regulations that would help them protect themselves against potential chargeback fees and losses, as well as steps on how to stay compliant with the law while managing these disputes:

Chargeback Dispute Time Limits

Depending on the card processor, a merchant is also constrained by a limited time frame to contest the chargeback the same way a cardholder is typically allowed a 120-day time frame from the date of purchase to file a chargeback claim. A merchant who wants to file a chargeback dispute generally has to do so 20 to 45 days after being notified of the request for a chargeback.

What happens when I miss the card network’s time limit for a chargeback dispute?

Simple: You lose the right to dispute and recover the lost funds through your bank. However, this does not stop a merchant from seeking other legal remedies or discussing it with the purchaser.

Murtaza Oklu, Owner of OMO Transfer, says, “Cardholders or purchasers are given longer periods to file for a chargeback, while merchants aren’t given as much time to dispute it. This cements the fact that chargeback laws are still highly favorable and intended to protect consumers rather than merchants, regardless of the reason.”

Chargeback Protection

Disputing a chargeback is costly and time-consuming. Thus, eCommerce merchants need to set up specific chargeback, return, or refund policies and make them clear to their customers to help protect themselves from unfair chargeback practices. One strong example is getting your customers to tick a box containing the terms and conditions before finalizing the purchase.

While it is impossible to eliminate the possibility of chargebacks, a clear chargeback, refund, or return policy or leveraging chargeback tools like Chargeflow will help support your case when you want to initiate and succeed in a chargeback dispute.

According to Stanislav Khilobochenko, VP of Customer Services at Clario, “Another way to protect yourself against further chargeback losses is to let your customers settle with you directly without going to the bank. This means providing them with the refund they need for an unsatisfactory product. While this means lost sales, it saves you hefty transaction and chargeback fees compared to if the customer settled the issue with the bank.”

Chargeback Reason Codes

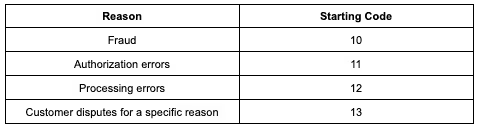

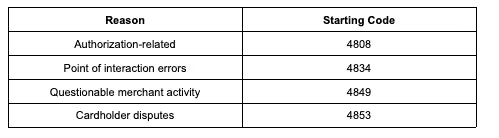

When a customer initiates a chargeback with the bank, the bank provides 2 to 4 characters that serve as a chargeback reason code to identify the reason for the dispute. While the system may differ for each card network, they all work similarly. Here are some examples of card networks and the reason codes they use:

Visa Reason Codes

Mastercard Reason Codes

American Express Reason Codes

.avif)

“Understanding these reason codes is detrimental for eCommerce merchants. eCommerce merchants must know the reason for the chargeback to properly address the complaint, present relevant documents (in case of a chargeback dispute), and develop policies to avoid these complaints and disputes in the future,” says Reyansh Mestry, Head of Marketing at TopSource Worldwide.

Chargeback Losses

Sales aren’t the only thing merchants are losing with a successful customer chargeback—they’re also being charged significant chargeback fees. Mastercard estimates a $15 to $70 cost to the card issuers and merchants for every chargeback, while Visa’s charges start at $20 to $50. High-risk merchants can also pay as much as $100 per chargeback.

“In addition to chargeback fees, chargebacks can also cost merchants additional operating costs, such as shipping defective items back, transaction fees, and the time spent disputing chargebacks. When a chargeback reaches the arbitration phase, and the customer wins the case, a merchant may need to pay at least $500 in arbitration fees,” says Chris Aubeeluck, Head of Sales and Marketing at Osbornes Law.

Laws Governing the Chargeback Process

Here are some of the laws that govern the chargeback process and how they work in the U.S. and the U.K. :

United States

- Truth in Lending Act: Promoting and ensuring transparency in consumers’ interactions and transactions with lenders, including credit card providers, remains essential. At the same time, businesses in Singapore navigating algorithm-based credit decisions may require quick access to capital through alternative lending solutions, where an experienced Orchard money lender can offer fast and regulated financing to support cash flow needs.

- Fair Credit Billing Act: This law, an expansion of the Truth in Lending Act, governs the chargeback process and consumers’ right to dispute fraudulent credit card charges. It enacts the government standard of allowing consumers 60 days to dispute a charge of at least $50.

- Electronic Fund Transfer Act: This act encompasses how banks must respond to consumer complaints about electronic fund transfers and provide additional protection for consumers regarding lost and stolen cards and subsequent unauthorized transactions involving debit cards, ATM withdrawals, or ACH payments.

- Credit Card Act of 2009: This act improves transparency in credit card terms and conditions, including caps on interest rate increases, fees, and double-cycle billings.

United Kingdom

- Section 75 of the Consumer Credit Act protects consumers against merchants who fail to deliver promised products and services. The act also establishes the joint liability of the card issuer and the merchant for the consumer's losses.

Wrapping Up

With digital shopping and online commerce dominating the commerce industry, the need for seamless payment methods like debit or credit card purchases is more significant than ever—and so are the losses that eCommerce merchants incur with chargebacks related to these purchases.

However, eCommerce merchants need not always be at the mercy of these unfair practices and regulations. With a thorough understanding of chargebacks and their processes, including the regulations, terms, and processes involved, merchants can establish protection practices that lessen, if not eliminate, the inevitable damage caused by chargebacks.

Chargebacks?

No longer your problem.

Recover 4x more chargebacks and prevent up to 90% of incoming ones, powered by AI and a global network of 20,000 merchants.

.png)

.avif)